It's the Great Singapore Sale again, and there has never been a better time to enjoy credit card promotions. Every bank seems determined to out-do each other in bigger discounts and better deals for cardholders in their tie-ups with merchants.

Card marketing has never seen tougher times of competition. Aside from the stiff competition in funding and delivering all kinds of expensive-to-run promotions (consumers have even come up with a ever-so-helpful listing of all the great credit card deals this year), customer loyalty seems to be a thing of the past as more and

How many credit cards do you carry with you? 4? 5? 10?

It is a sad, sad state of things to see a credit card reduced to a retail discount card.

In March 2011, OCBC Cards managed to complete the most large-scale loyalty platform implementation in recent memory. I was glad to be part of the project team to have made it happen.

In the time I have spent in customer loyalty, the primary focus had been on a few key elements, namely, the value of the reward currency, the relevance of the rewards earned, and the rate at which they are earned.

Back then, no one had anticipated the proliferation of social networking and the widespread use of the smart phone as a banking medium.

As these developments unfold in ever-increasing frequency and speed, it dawned on me, that a customer's view on rewards would also have altered by these changes. This is an epiphany that led me to think that the next battle ground in rewards is not in the 'earn', but the 'burn'.

While the rest of the card banking community tries to out-do each other in multiplier points earn, perhaps enabling a quick and easy way for customers to access their rewards currency anytime, anywhere, is the next big thing to disrupt the market?

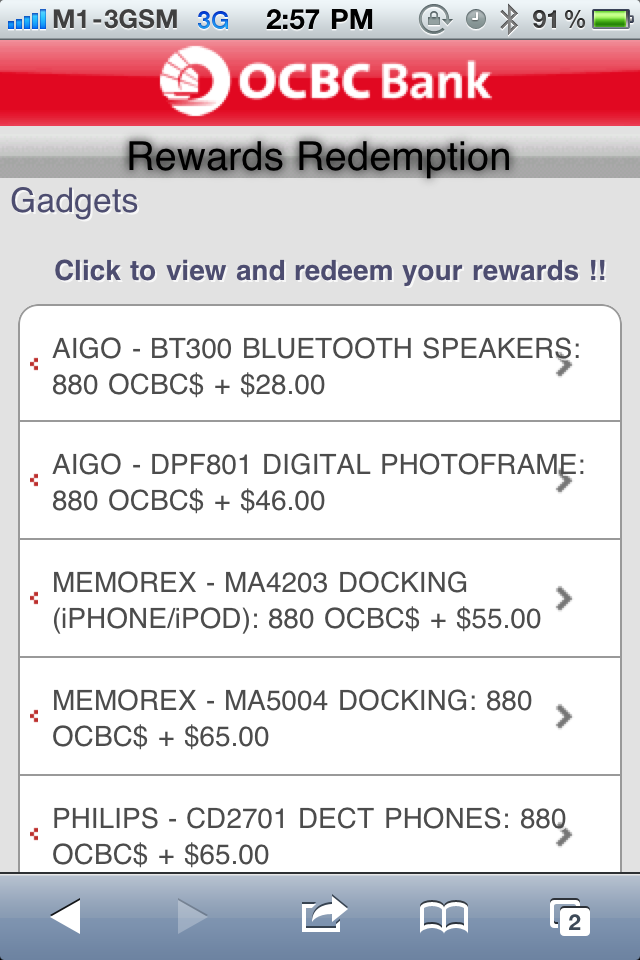

I hope anyone who reads this will take a moment to visit the OCBC rewards mobile website: mobile.ocbc.com.

Although this is a mobile web-based service at the moment, I hope that in time, our recently released Android mobile banking app will incorporate rewards as a key functionality.

Meanwhile, have a look a a video on the much-talked about OCBC Android mobile banking app.

ZDNet interview of mobile banking product manager.

This is something I recently found on Colloquy.com article.

Apparently, it's a clip from a futuristic-doomsday movie warning ourselves against fascism and 'big brother' future that seems to be approaching us very soon. That, of course, is the less-than-positive side of looking at the future. But, if we take a moment to assess the kinds of CRM capabilities we have today, it should not be impossible to do the things we see in the clip.

It does get hairy when good CRM is misused to the point when people think that respect for their privacy has been ignored. Information versus privacy -- the perennial battle in any CRM and loyalty marketing database.

This unplanned encounter was timed in a curious fashion. I had just been having conversations with veterans in the industry about how the banking world (especially in consumer finance) has underutilised the power of connectivity and community advocacy. So, this begs the question: Are banks really such seasoned creatures of habit that they are blinded by the speed with which the rest of the consumer world runs?

As a member of the industry, it is not difficult to appreciate the difficulties for banks to jump on the bandwagon with similar speeds as the world of the FMCG, travel, or even hospitality. The fact remains that as a financial institution (despite all the fuss about it as an investment vehicle) the bank is, ultimately, the custodian of assets of the people, a.k.a., common folk like you and I. For all that is said and done, a bank simply cannot proceed with any new initiatives without having to satisfy the arduous and sometimes painstaking process of due diligence.

However, as both a consumer and bank employee, I believe that some manner of agility can be achieved. Life simply cannot be as rigid as it used to be when we needed to bring a pass book and stand behind a tall counter before we can get to our own money.

The question of suitability in loyalty currency is the single most intriguing question that has never quite gotten a scientific and clinical treatment. In particular, I do not believe that any formal study has been conducted with regards to loyalty currency preference in payment cards.

I am of the opinion that, despite cultural and social disparities in different markets, there must be some partiality towards one type of loyalty currency to another.

One year ago, I would have agreed whole-heartedly. Today, my nerves are shaken a little, with added fuel by horror stories of the 'firing squad' from the Big Boy in the business.

Do I still find a joy in cards & payments challenging and meaningful? Absolutely.

Is there a future for cards? Of course - as long as consumerism exists.

Will 'cards' be the growth engine for payments? Probably not. Other form factors will emerge and gradually replace the card, given the world's increasing reliance on 'virtual-ism'.

So, question to self: Should we all start looking for new jobs?

Consumers in Singapore are spoilt for choices, particularly in credit card marketing offers. In fact, the rules here are so relaxed, that card marketing practices will never be allowed in places such as the US or Euro-zone.

Case in point: When was the last time you received a cheque from your credit card bank giving you 'free' money? (On that note, please send me examples of the cheques you have, please.)

Such predatory marketing tactics will soon be banned in the UK. The Euro-zone will likely follow at some point.